Contact us

Get Your Free Consultation

Initial consultations are free, and we offer evening and weekend appointments upon request. Let us know what you’re going through and we’ll reach out with your next steps.

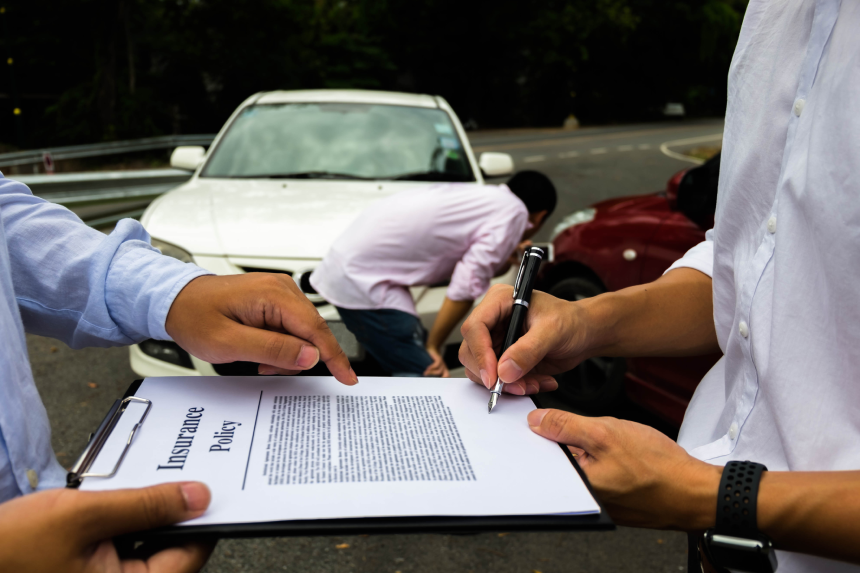

You get into a car crash caused by another driver and suffer an injury that’s going to keep you out of work for at least several weeks. You file an insurance claim against their policy in order to get compensation for your medical costs and lost wages, as well as the cost for repairing your vehicle or even replacing it if it wound up totaled in the crash.

Then, you receive a settlement offer, either in writing or over the phone. At first, you may have felt excited to hear from the insurance company, but that excitement turns to anger, frustration or even fear when you realize just how low their offer was. What do you do when the insurance company expects you to settle for far less than the cost of a significant motor vehicle crash?

Insurance companies have a responsibility to offer reasonable resolutions to a claim made by the victim of a crash that they should cover due to the liability of one of their policyholders. However, they do not have to make a settlement offer that exceeds the amount of coverage that the other driver had.

Learning a little bit about the policy held by the other driver can give you an idea about whether you have room for negotiation or whether the offer on the table is the highest amount possible. Or does it reflect a low-value insurance policy?

If a settlement offer is well below your current costs but also isn’t the maximum coverage level purchased by the other driver, you may be able to enter in negotiation with the insurance company. As previously noted, insurance companies are obligated under the law to follow through with their promises of protection for policyholders and those who get hurt by drivers whom they cover.

When an insurance company violates those obligations by denying a reasonable claim or making settlement offers that don’t begin to cover someone’s costs, they may have engaged in bad faith insurance practices that leave them open to claims or legal action in the future.

Sadly, it is not uncommon for victims of a car crash to learn that the other driver had very little insurance or no insurance at all. When that happens, insurance claims likely won’t be the solution, unless you have uninsured or underinsured driver protection on your personal vehicle policy.

Barring that situation, you may have to consider bringing a personal injury claim against the driver who caused the crash and did not have enough insurance to offset the liability that resulted from the collision.